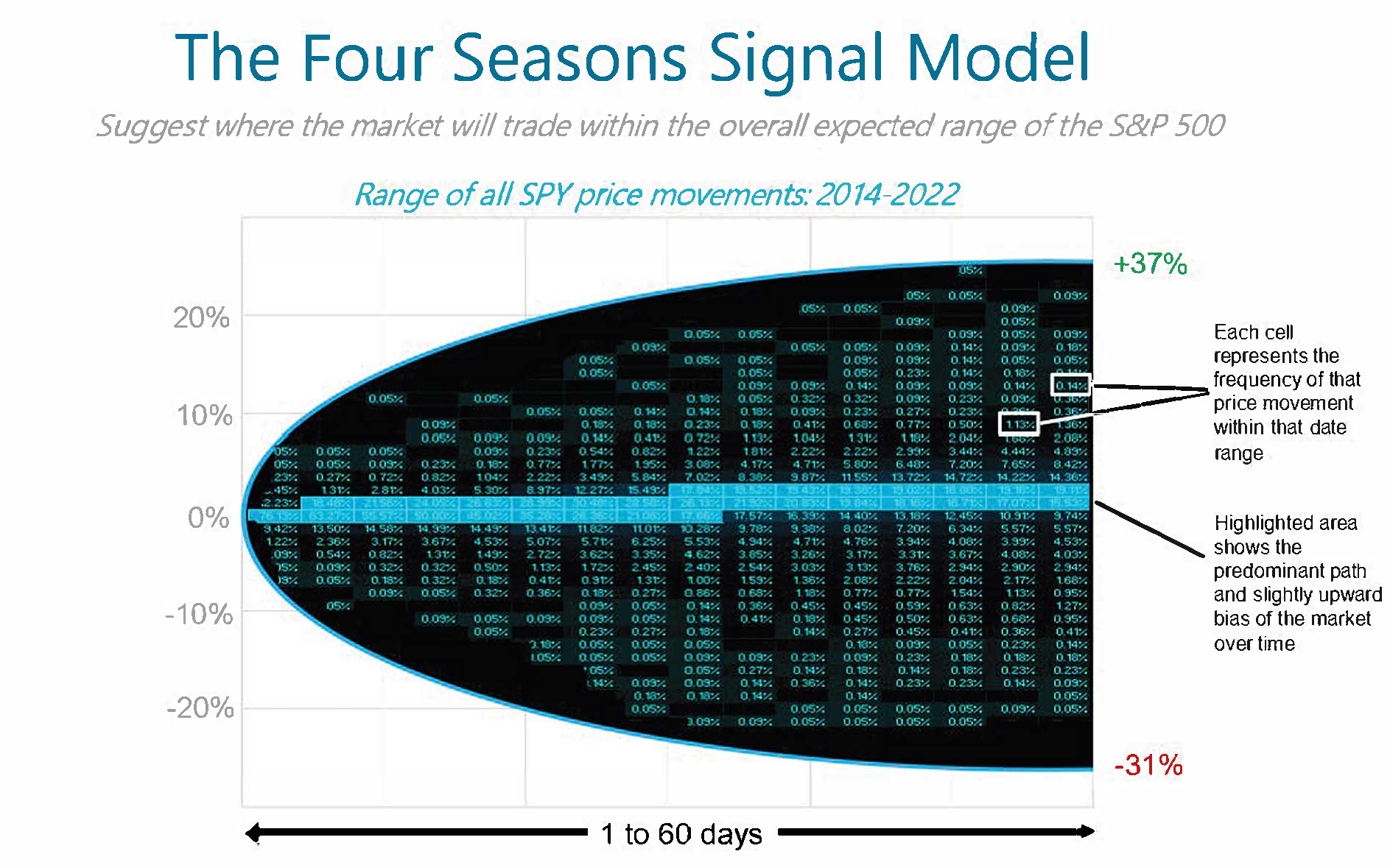

Projecting The Market’s Next Season

The Four Seasons strategy is a quantitative dynamic model that looks to identify both the direction of the broad market and the potential range of price movements. ZEGA uses 19 different volatility-based triggers that provide signals to indicate one of 4 seasons:

- Wide Bull

- Wide Bear

- Narrow Bull

- Narrow Bear

Portfolios are then created to capitalize on what we believe we’ve the identified as the current seasons by rotating allocations. The Four Seasons strategy comes in 5 different versions allowing investors to align their risk tolerance with the appropriate model. Exposure ranges from leveraged long to short exposure in the Aggressive versions, while the Moderate and Conservative models navigate between risk on and risk off.

Performance

Four Seasons Aggressive

| as of 5/31/2026 | MTD | YTD | 1 Year | 3 Year | 5 Year | 10 Year | ITD** |

| 4 Seasons Net* | 5.18% | 11.32% | 23.59% | 19.10% |

|

|

14.23% |

| Benchmark (S&P 500) | 5.26% | 11.26% | 29.78% | 23.62% | 14.15% | 15.65% |

Four Seasons Moderate - Aggressive

| as of 5/31/2026 | MTD | YTD | 1 Year | 3 Year | 5 Year | 10 Year | ITD** |

| 4 Seasons Net* | 5.17% | 10.83% | 23.56% | 17.39% |

|

|

15.16% |

| Benchmark (S&P 500) | 5.26% | 11.26% | 29.78% | 23.62% | 14.15% | 15.65% |

|

Four Seasons Moderate

| as of 5/31/2026 | MTD | YTD | 1 Year | 3 Year | 5 Year | 10 Year | ITD** |

| 4 Seasons Net* | 3.51% | 7.49% | 16.67% | 12.44% |

|

|

10.68% |

| Benchmark (Target Risk) |

2.80% | 7.65% | 20.22% | 14.93% |

|

|

|

Four Seasons Moderate - Conservative

| as of 5/31/2026 | MTD | YTD | 1 Year | 3 Year | 5 Year | 10 Year | ITD** |

| 4 Seasons Net* | 2.25% | 4.98% | 10.95% | 10.32% |

|

|

8.98% |

| Benchmark (Agg) | 0.31% | 0.38% | 5.14% | 3.95% |

|

Four Seasons Conservative

| as of 5/31/2026 | MTD | YTD | 1 Year | 3 Year | 5 Year | 10 Year | ITD** |

| 4 Seasons Net* | 1.59% | 3.70% | 8.31% | 8.34% |

|

|

7.54% |

| Benchmark (Agg) | 0.31% | 0.38% | 5.14% | 3.95% |

|

*Note: Returns are expressed in US Dollars and calculated net of actual fees. Performance includes reinvestment of dividends and other earnings.

**Note: Inception-to-date (ITD) are shown on an annualized basis

ZEGA Investments is a registered investment adviser and investment manager that specializes in derivatives. ZEGA is a separate accounts manager and all returns expressed herein are solely from the separate accounts business within ZEGA.

The 4 Seasons Models are tactical models that take positions in S&P 500 based ETFs as well as short-term US Treasury ETFs to capture market movement. The positions in each of the 4 Seasons model will depend on the risk profile for that specific strategy. Investors should consider, along with other factors, their specific risk tolerance in evaluating these strategies. These strategies use a predicative model that aims to project the direction and volatility of the stock market. The strategies identify both bullish/bearish bias. The methodology projects high/low magnitude moves as well as market direction the next one to sixty days. The composite includes all portfolios that were at least 70% dedicated to this strategy. Depending on the 4 Season model, The following benchmarks are used: 1) the S&P 500 2) the S&P 500 Target Risk Growth or 3) The Barclays US Aggregate Bond Index . The S&P 500 Index is a collection of 500 of the largest publicly traded US Equity large cap companies. The S&P Target Risk Growth Index is designed to measure the performance of equity allocations, while seeking to provide limited fixed income exposure to diversify risk. The Barclays US Aggregate Bond Index. is a market cap weighted index of fixed income securities, and is widely considered the most used index in the fixed income investment community. The minimum account size for this composite is $10,000. ZEGA Investments claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. ZEGA has not been independently verified.

All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is no guarantee of future results and there can be no assurance, and clients should not assume, that the future performance of any of the model portfolios will be comparable to past performance.

These results should not be viewed as indicative of the advisor’s skill. The prior performance figures indicated herein represent portfolio performance for only a short time period and may not be indicative of the returns or volatility each portfolio will generate over a long time period. The performance presented should also be viewed in the context of the broad market and general economic conditions prevailing during the periods covered by the performance information.

The actual results for the comparable periods would also have varied from the presented results based upon the timing of contributions and withdrawals from individual client accounts. The performance figures contained herein should be viewed in the context of the various risk/return profiles and asset allocation methodologies utilized by the asset allocation strategists in developing their model portfolios and should be accompanied or preceded by the model. Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. In finance, standard deviation is applied to the annual rate of return of an investment to measure the investment's volatility.